library(plotly)

# ── Zone centroids (approximate geographic centres) ──────────────────

zone_coords <- tribble(

~zone, ~lat, ~lon, ~label,

"DE_LU", 51.0, 10.0, "DE-LU",

"FR", 46.5, 2.5, "FR",

"NL", 52.0, 5.5, "NL",

"BE", 50.8, 4.5, "BE",

"AT", 47.5, 14.0, "AT",

"DK_1", 56.0, 9.5, "DK1",

"DK_2", 55.5, 12.0, "DK2",

"NO_1", 60.0, 10.5, "NO1",

"NO_2", 59.0, 6.0, "NO2",

"NO_3", 63.5, 10.5, "NO3",

"NO_4", 68.0, 15.5, "NO4",

"NO_5", 60.5, 6.5, "NO5",

"SE_1", 66.0, 18.0, "SE1",

"SE_2", 63.0, 16.0, "SE2",

"SE_3", 59.0, 16.0, "SE3",

"SE_4", 56.5, 14.5, "SE4",

"FI", 62.0, 26.0, "FI"

)

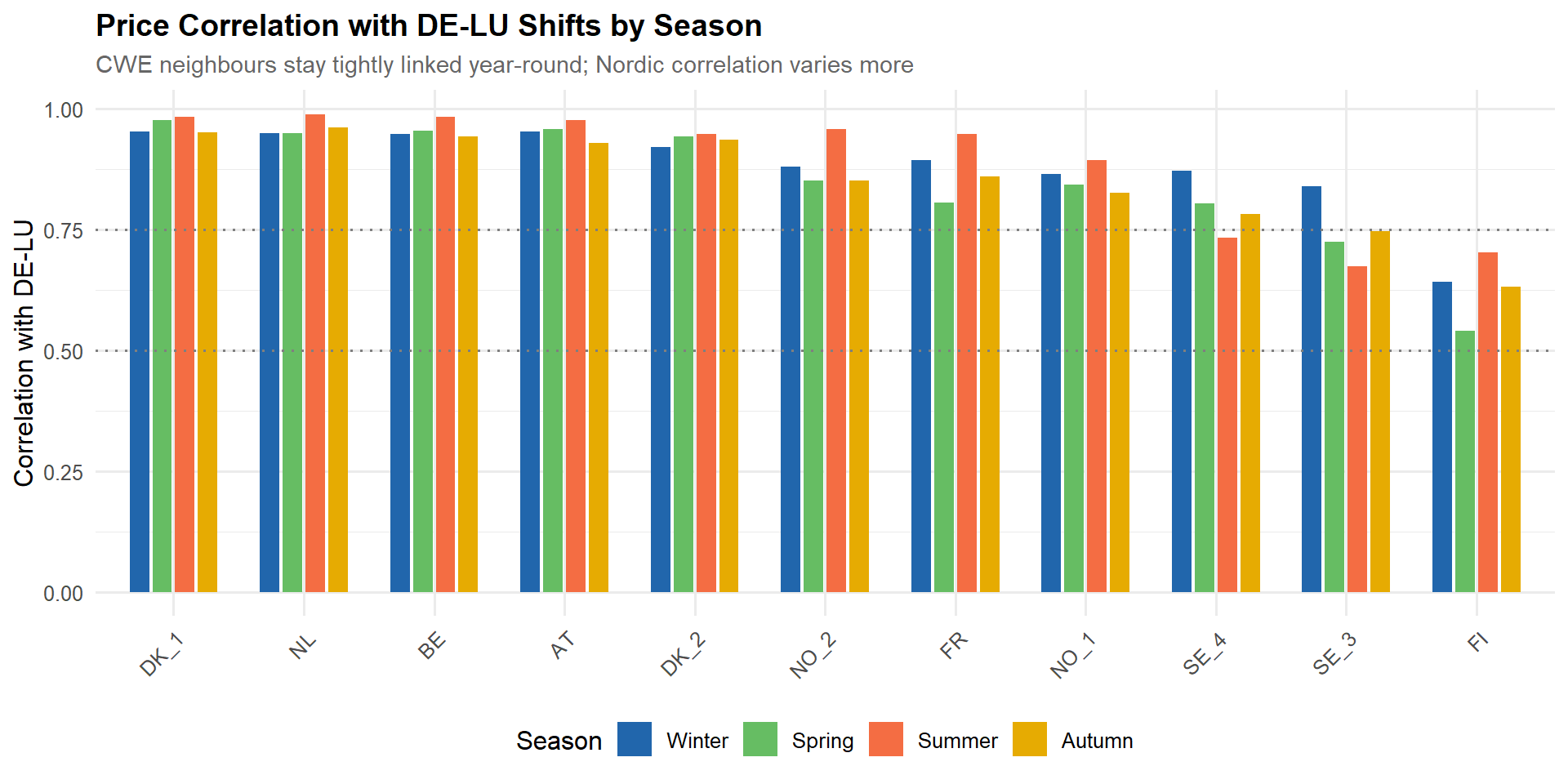

# ── DE-LU correlations ──────────────────────────────────────────────

delu_corr <- tibble(

zone = rownames(price_matrix),

corr_de_lu = price_matrix[, "DE_LU"]

) |>

filter(zone != "DE_LU") |>

left_join(zone_coords, by = "zone")

delu_point <- zone_coords |> filter(zone == "DE_LU")

# ── Colour mapping (sequential warm) ────────────────────────────────

corr_to_colour <- colorRamp(c("#F7F7F7", "#FDDBC7", "#EF8A62", "#B2182B"))

delu_corr <- delu_corr |>

mutate(

colour_rgb = map_chr(corr_de_lu, \(x) {

rgb_vals <- corr_to_colour(x)

sprintf("rgb(%d,%d,%d)",

round(rgb_vals[1]), round(rgb_vals[2]), round(rgb_vals[3]))

}),

hover_text = paste0(

"<b>", label, "</b><br>",

"Correlation with DE-LU: <b>", sprintf("%.2f", corr_de_lu), "</b>"

)

)

# ── Country-level averages for choropleth background ────────────────

zone_to_iso3 <- tribble(

~zone, ~iso3,

"FR", "FRA", "NL", "NLD", "BE", "BEL", "AT", "AUT",

"DK_1", "DNK", "DK_2", "DNK",

"NO_1", "NOR", "NO_2", "NOR", "NO_3", "NOR", "NO_4", "NOR", "NO_5", "NOR",

"SE_1", "SWE", "SE_2", "SWE", "SE_3", "SWE", "SE_4", "SWE",

"FI", "FIN"

)

country_corrs <- delu_corr |>

left_join(zone_to_iso3, by = "zone") |>

group_by(iso3) |>

summarise(corr_de_lu = mean(corr_de_lu), .groups = "drop") |>

bind_rows(tibble(iso3 = "DEU", corr_de_lu = 1.0))

# ── Build plotly geo map (responsive sizing) ──────────────────────────

fig <- plot_geo(height = 700) |>

# Choropleth background — country polygons filled by correlation

add_trace(

type = "choropleth",

locations = country_corrs$iso3,

z = country_corrs$corr_de_lu,

colorscale = list(

c(0, "rgb(222,235,247)"),

c(0.25, "rgb(247,247,247)"),

c(0.5, "rgb(253,208,162)"),

c(0.75, "rgb(227,120,71)"),

c(1, "rgb(178,24,43)")

),

zmin = 0.15, zmax = 1,

marker = list(line = list(color = "rgb(180,180,180)", width = 1)),

colorbar = list(title = "Correlation", len = 0.4, y = 0.5),

hoverinfo = "none",

showlegend = FALSE

) |>

layout(

title = list(

text = "How Correlated Are European Electricity Prices with Germany?",

font = list(size = 16)

),

geo = list(

scope = "europe",

projection = list(type = "mercator"),

lonaxis = list(range = c(-5, 30)),

lataxis = list(range = c(44, 72)),

showland = TRUE, landcolor = "rgb(235,235,235)",

showocean = TRUE, oceancolor = "rgb(225,235,245)",

showcountries = TRUE, countrycolor = "rgb(180,180,180)",

showlakes = TRUE, lakecolor = "rgb(225,235,245)",

showcoastlines = TRUE, coastlinecolor = "rgb(180,180,180)",

resolution = 50

),

showlegend = FALSE,

autosize = TRUE,

margin = list(t = 60, b = 20)

)

# ── Connection lines from DE-LU to each zone ────────────────────────

for (i in seq_len(nrow(delu_corr))) {

row <- delu_corr[i, ]

fig <- fig |>

add_trace(

type = "scattergeo", mode = "lines",

lon = c(delu_point$lon, row$lon),

lat = c(delu_point$lat, row$lat),

line = list(

width = row$corr_de_lu * 4,

color = row$colour_rgb

),

opacity = 0.9,

hoverinfo = "none",

showlegend = FALSE

)

}

# ── Zone markers (sized and coloured by correlation) ─────────────────

fig <- fig |>

add_trace(

type = "scattergeo", mode = "markers+text",

data = delu_corr,

lon = ~lon, lat = ~lat,

marker = list(

size = ~corr_de_lu * 25 + 5,

color = ~colour_rgb,

line = list(width = 1.5, color = "white")

),

text = ~paste0(label, " (", sprintf("%.2f", corr_de_lu), ")"),

textposition = "top center",

textfont = list(size = 10, color = "rgb(50,50,50)"),

hovertext = ~hover_text,

hoverinfo = "text",

showlegend = FALSE

)

# ── DE-LU reference marker ──────────────────────────────────────────

fig <- fig |>

add_trace(

type = "scattergeo", mode = "markers+text",

lon = delu_point$lon, lat = delu_point$lat,

marker = list(

size = 16, color = "#B2182B", symbol = "diamond",

line = list(width = 2, color = "white")

),

text = "DE-LU", textposition = "top center",

textfont = list(size = 12, color = "black", family = "Arial"),

hovertext = "<b>DE-LU</b><br>Reference zone",

hoverinfo = "text",

showlegend = FALSE

)

fig